Credit utilisation is one of the most misunderstood concepts in personal finance, yet it is the second most important factor in determining your credit score. If you are struggling to improve your rating despite making all your payments on time, your credit utilisation ratio is almost certainly the culprit.

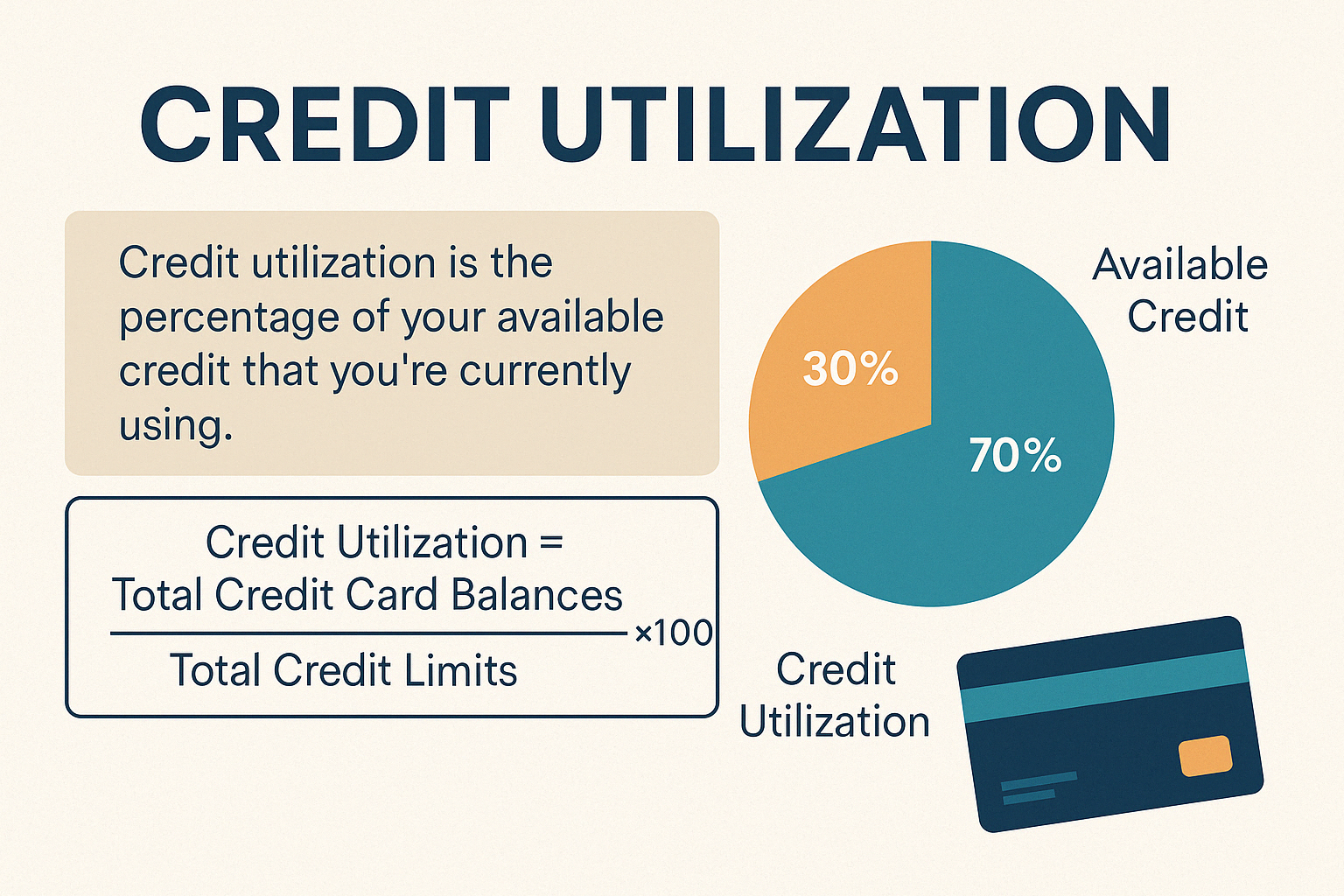

Simply put, credit utilisation is the percentage of your available credit limit that you are currently using. Lenders look closely at this figure because it provides a clear snapshot of your reliance on borrowed money. A high utilisation ratio suggests you are stretched financially, making you a higher risk to new lenders.

How to Calculate Your Utilisation Ratio

Calculating your ratio is straightforward. You divide your total outstanding credit card balances by your total available credit limits, then multiply by 100 to get a percentage.

For example, if you have a single credit card with a limit of £2,000 and your current balance is £1,000, your utilisation ratio is 50%. If you have two cards with a combined limit of £5,000 and total balances of £4,500, your ratio is a dangerously high 90%.

Credit reference agencies calculate this ratio across all your revolving credit accounts combined, but they also look at the utilisation on individual cards. Maxing out one card while leaving another empty will still negatively affect your score.

The 30% Rule for Credit Scores

Financial experts universally recommend keeping your credit utilisation below 30%. Lenders view consumers who use less than a third of their available credit as responsible borrowers who manage their finances well. If you can keep your ratio below 10%, you will see an even greater positive impact on your credit score.

When your utilisation creeps above 50%, your score will begin to drop significantly. If you max out your cards (reaching 90% to 100% utilisation), lenders will view you as highly distressed, and your applications for new credit are likely to be rejected, even if you have never missed a payment.

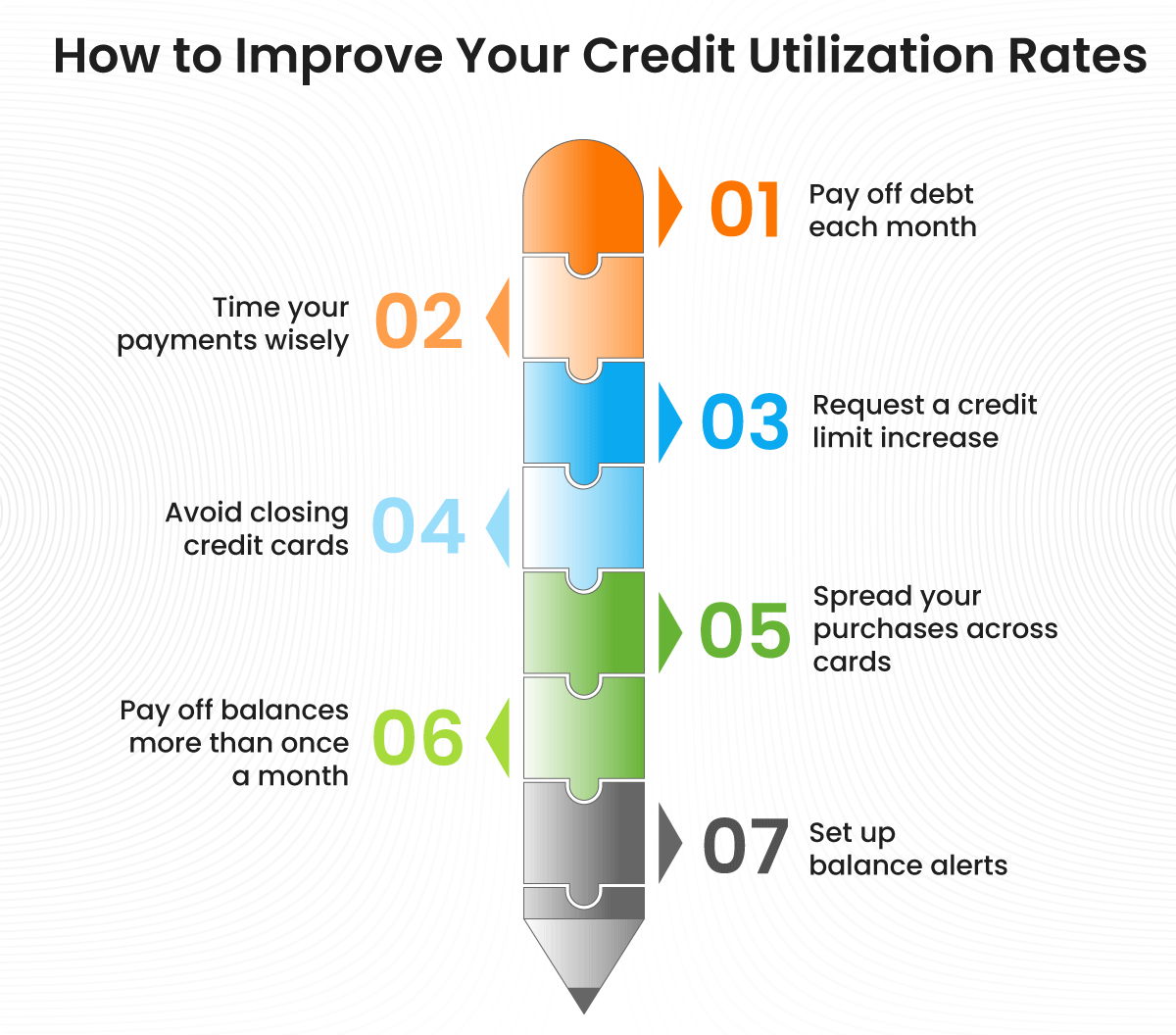

Two Fast Ways to Lower Your Ratio

The most obvious way to lower your utilisation is to pay down your balances. Even making an extra payment mid-month before your statement is generated can dramatically reduce the balance reported to the credit reference agencies.

The second method is to request a credit limit increase from your current lender. If your limit increases from £2,000 to £4,000, but your balance remains at £1,000, your utilisation ratio instantly drops from 50% to 25%. However, you must be disciplined enough not to spend the new available credit, otherwise you will end up in a worse financial position.

Update: Check Your Eligibility Today

Click the button below to view your updated credit score and identify any potential errors instantly.

CHECK YOUR CREDIT SCORE NOW*Secure, 256-bit encrypted connection.