Every time a company looks at your credit report, they leave a digital footprint. However, not all footprints are created equal. Understanding the difference between a hard search and a soft search is vital for protecting your credit score and ensuring you are approved for the best financial products.

Many consumers inadvertently damage their credit rating by applying for multiple credit cards or loans in a short period, unaware that each application leaves a lasting mark. By learning how to navigate these searches, you can shop around for the best deals without penalising yourself.

What is a Soft Search?

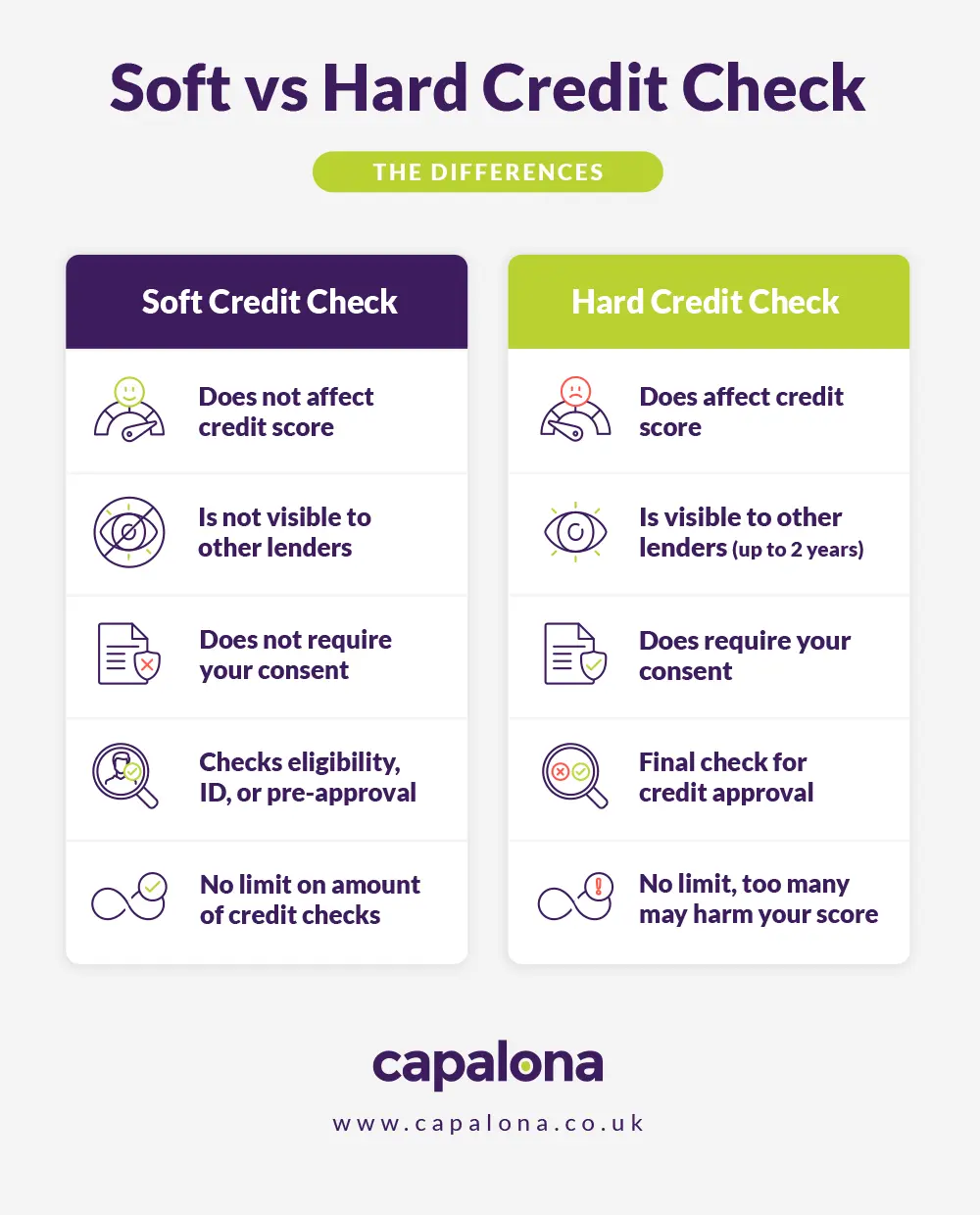

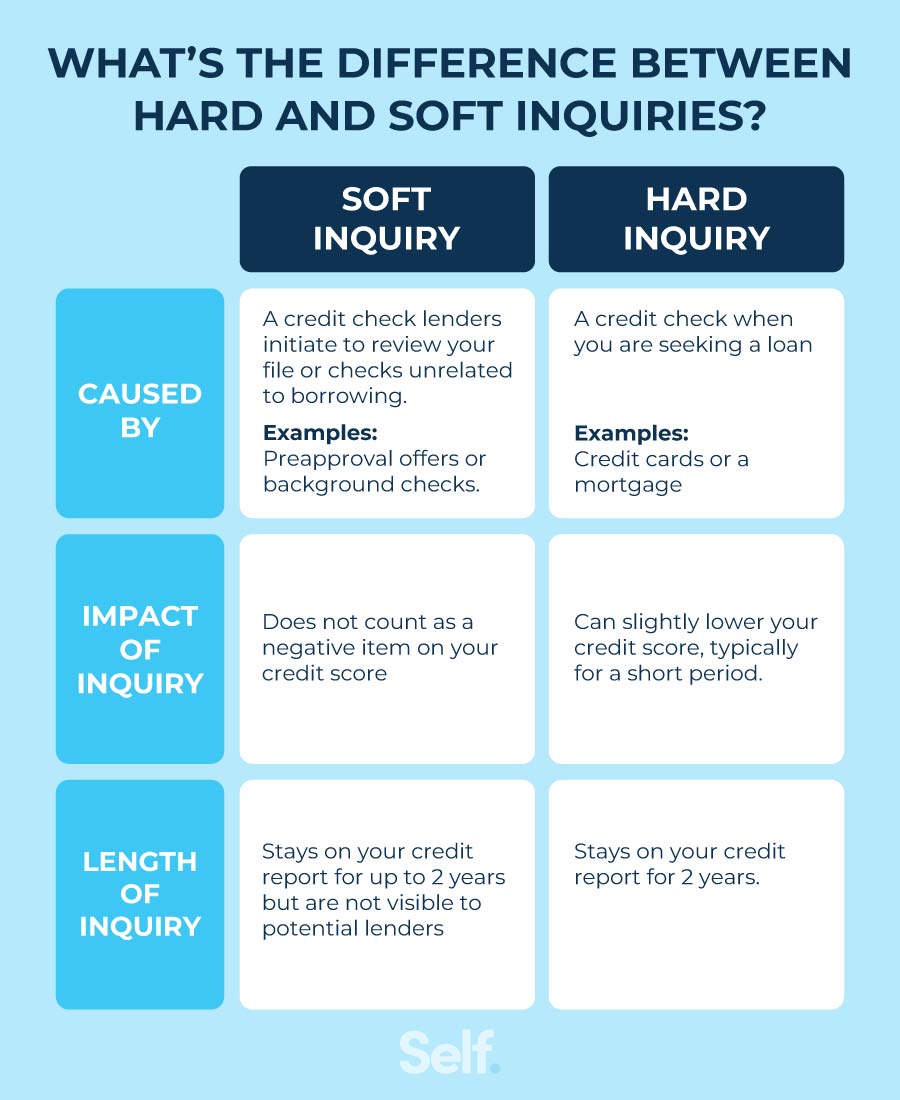

A soft search is a preliminary look at your credit report. It is used to check your identity, verify your address, or determine your eligibility for a product before you formally apply. Crucially, a soft search does not affect your credit score.

You can see soft searches when you check your own file, but lenders cannot see them. This means you can have hundreds of soft searches on your report without any negative consequences. Common examples of soft searches include checking your own score via a free credit report service, using an eligibility checker on a comparison website, or when an employer conducts a background check.

What is a Hard Search?

A hard search occurs when you make a formal application for credit, such as a mortgage, personal loan, credit card, or mobile phone contract. The lender conducts a deep dive into your financial history to make a final lending decision.

Unlike soft searches, a hard search leaves a visible footprint on your file that other lenders can see. This footprint remains on your report for 12 months (or longer for debt collection searches). More importantly, a hard search will slightly lower your credit score.

The Danger of Multiple Hard Searches

One or two hard searches a year is perfectly normal and will not cause long-term damage. However, multiple hard searches within a short timeframe signal to lenders that you are desperate for credit. If you are rejected for a loan and immediately apply for three more, the subsequent lenders will see the recent hard searches, assume you are in financial distress, and reject you as well.

To protect your score, always use eligibility checkers (which only perform soft searches) to find out if you are likely to be accepted before you submit a formal application. Space out your applications by at least three to six months to allow your score time to recover from the initial hard search impact.

Update: Check Your Eligibility Today

Click the button below to view your updated credit score and identify any potential errors instantly.

CHECK YOUR CREDIT SCORE NOW*Secure, 256-bit encrypted connection.