A late payment marker on your credit report can feel like a heavy burden, especially if you are planning to apply for a mortgage or a significant loan. Many people search for ways to remove these negative marks before the standard six-year period expires. The truth is, removing a late payment is difficult, but it is not always impossible.

If the late payment is accurate, meaning you genuinely missed the payment, the lender is legally required to report it. Credit reference agencies must maintain an accurate reflection of your borrowing history. However, there are specific circumstances where you can successfully get a late payment removed.

Disputing Inaccurate Late Payments

The most common reason a late payment is removed is because it was recorded in error. If you paid on time but the lender processed the payment late due to an administrative error on their side, you have strong grounds for a dispute. You must gather your bank statements proving the money left your account on or before the due date.

Submit this evidence to both the lender and the credit reference agency. Once they verify the error, the late payment marker will be deleted from your file, and your credit score should recover. This is your strongest legal right and the most reliable route to removal. For a template you can use, see our free dispute letter template.

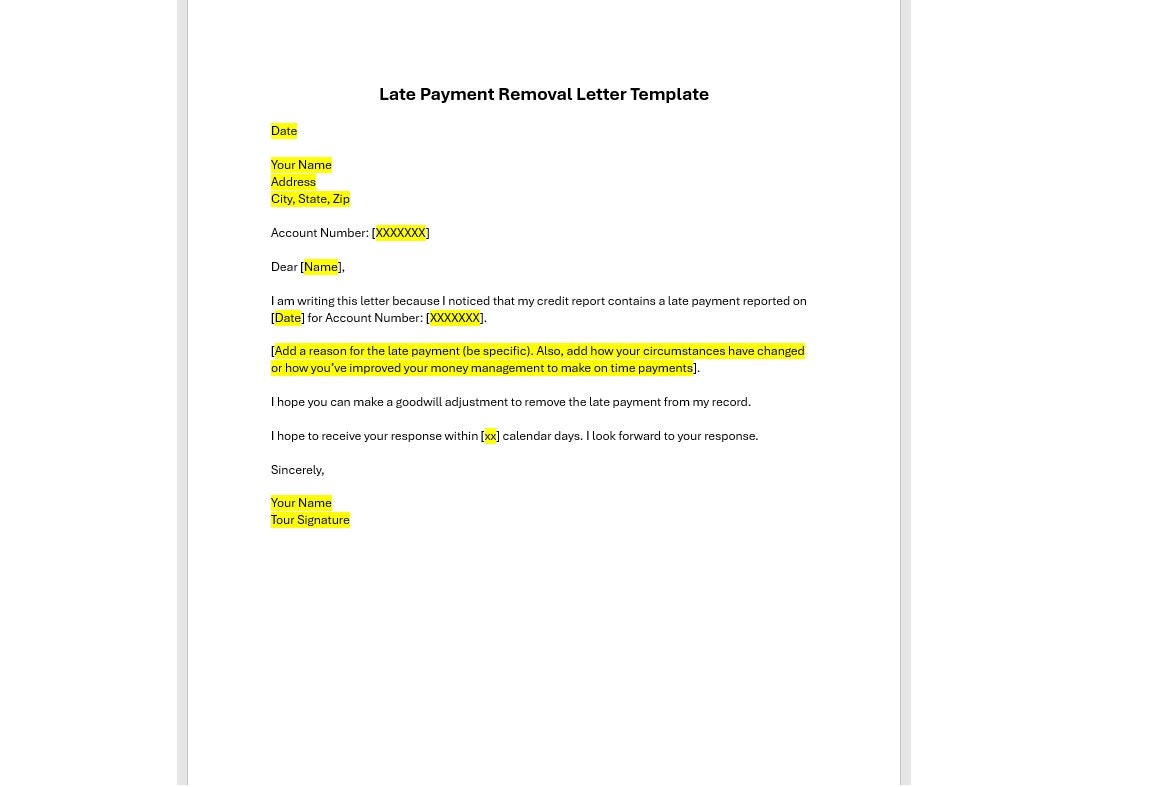

Writing a Goodwill Letter

If the late payment was genuinely your fault but was an isolated incident caused by exceptional circumstances, you can try writing a goodwill letter. This involves contacting the lender, explaining why you missed the payment (such as a sudden illness, redundancy, or bereavement), and politely asking them to remove the marker as a gesture of goodwill.

Lenders are not legally obligated to agree to this request. However, if you have been a loyal customer with an otherwise spotless payment history, some lenders will show leniency. Keep the letter professional, take responsibility for the missed payment, and clearly explain the mitigating circumstances. Avoid being confrontational or making demands.

What Happens If the Lender Refuses

If the lender declines your goodwill request and the late payment was genuinely your fault, you will need to wait for the six-year period to expire. In the meantime, focus on building a strong positive payment history. Set up direct debits for all your bills to ensure you never miss another payment. Over time, recent positive behaviour will outweigh older negative markers in the eyes of most lenders.

You should also check whether the late payment is correctly recorded. Sometimes lenders record the wrong date or the wrong account. If you spot any inaccuracy in how the marker is recorded, you can raise a formal dispute even if the underlying missed payment was real.

Update: Check Your Eligibility Today

Click the button below to view your updated credit score and identify any potential errors instantly.

CHECK YOUR CREDIT SCORE NOW*Secure, 256-bit encrypted connection.