Credit cards are incredibly useful financial tools, but they are also highly profitable products for the banks that issue them. Lenders employ various tactics to encourage you to borrow more and pay maximum interest. Understanding these strategies is essential to managing your credit card effectively and avoiding unnecessary costs.

Many consumers fall into expensive traps simply because they do not read the fine print or understand how credit card interest works. By recognising these common tactics, you can use your credit card to your advantage without paying unnecessary fees or interest charges.

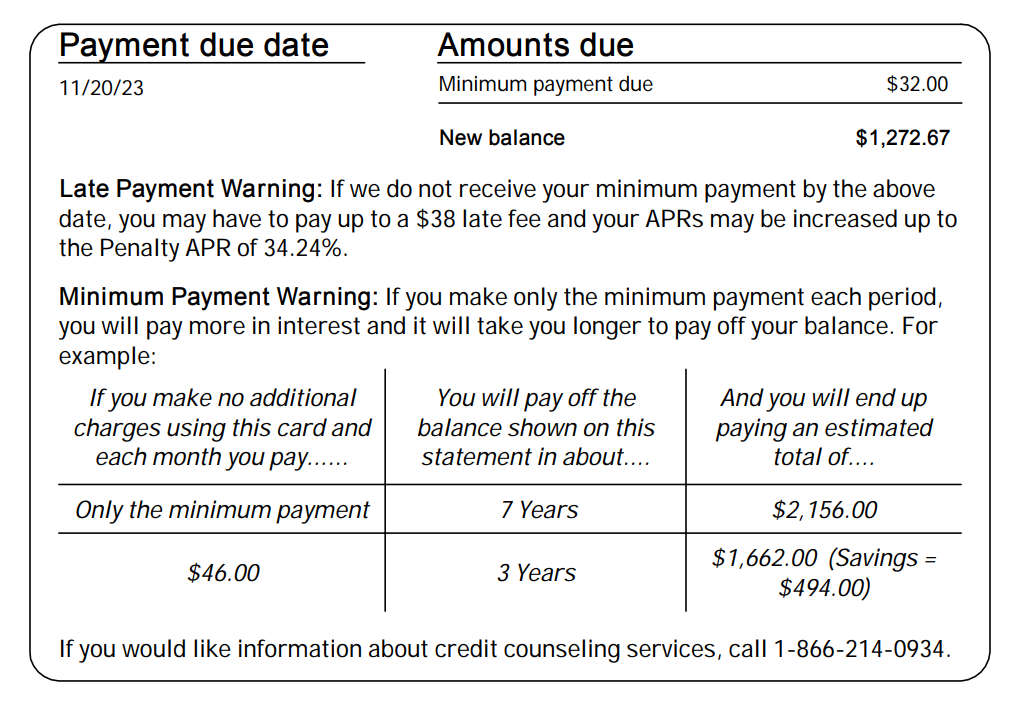

The Minimum Payment Trap

The most common and costly tactic is the minimum payment requirement. Credit card statements prominently display the minimum amount you must pay each month, which is typically just 1% to 2% of your outstanding balance, or a fixed amount such as £25. While paying the minimum keeps your account in good standing and prevents a missed payment marker on your credit report, it barely covers the interest charges.

If you only make minimum payments on a £2,000 balance at a typical interest rate of 22%, it can take over 20 years to clear the debt, and you will pay more than £4,000 in interest alone. Always aim to pay off your full balance each month. If that is not possible, pay as much above the minimum as you can afford.

0% Balance Transfer Pitfalls

0% balance transfer offers are a legitimate way to clear debt without paying interest, but they come with strict conditions that lenders rely on you not reading carefully. The most significant cost is the transfer fee, which is usually between 1% and 3% of the amount you move. You must calculate whether this fee is outweighed by the interest savings.

More importantly, if you miss a single monthly payment during the promotional period, the lender will instantly withdraw the 0% rate and revert your balance to the standard interest rate, which can be 20% or higher. Always set up a direct debit for at least the minimum payment to ensure you never miss a payment, and aim to clear the full balance before the promotional period ends.

Introductory Purchase Rates and Rate Increases

Many credit cards offer a 0% introductory rate on new purchases for a set period. Once this period ends, the rate jumps to the standard APR. Lenders count on cardholders carrying a balance past this point and paying the full interest rate on the remaining amount.

Lenders also have the right to increase your interest rate with 60 days notice. If you receive a notice of a rate increase, you have the right to reject it and close the account at the existing rate. However, you must stop using the card and repay the balance under the original terms.

Update: Check Your Eligibility Today

Click the button below to view your updated credit score and identify any potential errors instantly.

CHECK YOUR CREDIT SCORE NOW*Secure, 256-bit encrypted connection.